THE BASICS OF REAL OPTIONS

- By Admin

- June 15, 2014

- Comments Off on THE BASICS OF REAL OPTIONS

THE BASICS OF REAL OPTIONS

Real-life conditions are fraught with uncertainty and risks. Understanding the knowledge inherent in and accounting for the effects of these uncertainties is crucial to successful management. When uncertainty becomes resolved through the passage of time, actions, and events, decision makers can make the appropriate midcourse corrections by applying the knowledge gained and making decisions along flexible strategies. Strategic Real Options is a discipline that incorporates this learning model and permits the decision maker to take advantage of the full range of options, whereas traditional analyses that neglect this strategic flexibility will grossly undervalue certain capabilities, projects, and strategies.

How much is a platform technology really worth when its initial costs are high and it is delivered with lower than desired initial capabilities, but with the potential for significant flexibility for future add-ons? Should the organization build, buy, or lease a new untested technology? Is running a proof of concept a better strategy than executing large-scale acquisitions immediately a better strategy? How is a firm’s capability extended with flexible manufacturing systems? Is a modular open architecture really worth the added costs?

The Strategic Real Options approach helps answer these questions, and more, by estimating the value of strategic flexibility in a common and objective way across various alternatives and expressing the return on investment (ROI) of each option.These ROI estimates across the portfolio of alternatives provide the inputs necessary to predict the value of various options for accomplishing the firm’s goals such as risk hedging and reduction, and profit maximization. Integrated Risk Management (IRM) incorporates risks, budget constraints, reallocation options, and total ownership costs in recommending a defensible path forward. This approach identifies risky projects and programs while projecting immediate and future cost savings, total lifecycle costs, flexibility alternatives, critical success factors, and portfolio optimization, while controlling for cost overruns and schedule delays. IRM provides an optimized portfolio of capability options while maintaining the value of strategic flexibility. The IRM approach incorporates multiple Nobel-prize winning and well-established theories and applications in corporate finance, investments, economics, statistics, mathematics, and decision sciences into a comprehensive and flexible process that is defensible, replicable, scalable, and extensible to all areas of the firm.

TYPES OF REAL OPTIONS

Option to Wait and Execute: Buy additional time to wait for new information by prenegotiating pricing and other contractual terms to obtain the option but not the obligation to purchase or execute something in the future should conditions warrant it (wait and see

before executing).

- Run a Proof of Concept first to better determine the costs and schedule risks of a project versus jumping in right now taking the risk

- Build, Buy, or Lease. Develop internally or using commercially available technology or products

- Multiple Contracts in place that may or not be executed

- Market Research to obtain valuable information before deciding Venture Capital small seed investment with right of first refusal before executing large-scale financing

- Relative values of Strategic Analysis of Alternatives or Courses of Action while considering risk and the Value of Information

- Contract Negotiations with vendors, acquisition strategy with industrialbased ramifications (competitive sustainment and strategic capability and availability)

- Project Evaluation and Capability ROI modeling

- Capitalizing on other opportunities while reducing large-scale implementation risks, and determining the value of Research & Development (parallel implementation of alternatives while waiting on technical success of the main project, and no need to delay the project because of one bad component in the project)

- Low Rate Initial Production, Prototyping, Advanced Concept Technology Demonstration before full-scale implementation Right of First Refusal contracts

- Value of Information by forecasting cost inputs, capability, schedule, and other metrics

- Hedging and Call- and Put-like options to execute something in the future with agreed upon terms now, OTC Derivatives (Price, Demand,Forex, Interest Rate forwards, futures, options, swaptions for hedging)

Abandonment Option: Hedge downside risks and losses by being able to salvage some value of a failed project or asset that is out-of-the-money (sell intellectual property and assets, abandon and walk away from a project, buyback/sellback provisions).

- Exit and Salvage assets and intellectual property to reduce losses

- Divestiture and Spin-off

- Buyback Provisions in a contract

- Stop and Abandon before executing the next phase<./li>

- Termination for Convenience

- Early Exit and Stop Loss Provisions in a contract

Expansion Option: Take advantage of upside opportunities by having existing platform,

structure, or technology that can be readily expanded (utility peaking plants, larger oil platforms, early leapfrog technology development, larger capacity or technology-in-place for future expansion).

- Platform Technologies

- Mergers and Acquisitions

- Built-in Expansion Capabilities

- Geographical, Technological, and Market Expansion

- Foreign Military Sales

- Reusability and Scalability

Contraction Option: Reduce downside risk but still participate in reduced benefits (counter party takes over or joins in some activities to share profits but at the same time reduce your firm’s risk of failure or severe losses in a risky but potentially profitable venture).

- Outsourcing, Alliances, Contractors, Leasing

- Joint Venture

- Foreign Partnerships

- Co-Development and Co-Marketing

Portfolio Options: Combinations of options and strategic flexibility within a portfolio of nested options (path dependencies, mutually exclusive/inclusive, nested options).

- Determining the portfolio of projects’ capabilities to develop and field within Budget and Time Constraints, and what new Product Configurations to develop or acquire to field certain capabilities

- Allows for different Flexible Pathways: Mutually Exclusive (P1 or P2 but not both), Platform/Prerequisite Technology (P3 requires P2, but P2 can be stand-alone; expensive and worth less if considered by itself without accounting for flexibility downstream options it provides for the next phase), expansion options, abandonment options, parallel development or simultaneous compound options

- Determining the Optimal Portfolios given budget scenarios that provide the maximum capability,

flexibility, and cost effectiveness with minimal risks - Determining testing required in Modular Systems, mean-time-to-failure estimates, Replacement and Redundancy requirements

Relative value of strategic Flexibility Options:(options to Abandon, Choose, Contract, Expand, Switch, and Sequential Compound Options, Barrier Options, and many other types of Exotic Options)

- Maintaining Capability and Readiness Levels

- Product Mix, Inventory Mix, Production Mix

- Capability Selection and Sourcing

Sequential Options: Significant value exists if you can phase out investments over time, thereby reducing the risk of a one-time up-front investment (pharmaceutical and high technology development and manufacturing usually comes in phases or stages).

- Stage-gate implementation of high-risk project development, prototyping, low-rate-initial-production, technical feasibility tests, technology demonstration competitions

- Government contracts with multiple stages with the option to abandon at any time and valuing Termination for Convenience, and built-in flexibility to execute different courses of action at specific stages of development

- P3I, Milestones, R&D, and Phased Options

- Platform technology

Simultaneous Compound Options: Execute on multiple fronts at once to hedge the risk of choosing the wrong path and be susceptible to significant losses.

- Simultaneous Parallel Development to reduce critical path/schedule risk

- Simultaneous test programs to hedge executing or choosing the wrong path and to provide Flexibility to Choose (aircraft flight demonstrations, contract competition)

Switching Options: Ability to choose among several options, thereby improving

strategic flexibility to maneuver within the realm of uncertainty (maintain a foot in one door while exploring another to decide if it makes sense to switch or stay put).

- Ability to Switch among various raw input materials to use when prices of each raw material fluctuates significantly

- Readiness and capability risk mitigation by switching vendors in an Open Architecture through Multiple Vendors and Modular Design

OTHER OPTIONS: Barrier Options, Custom Options, Employee Stock Options, Exotic Options, Options Embedded Contracts, Options with Blackout Vesting Provisions, Options with Market Provisions and Change of Control Provisions, and many others.

Overview

Risk is not always a bad thing. In fact, when risks can be reduced and converted into opportunities, significant profits can be made. Real-life business conditions are fraught with uncertainty and risks. Understanding the knowledge inherent in and accounting for the effects of these uncertainties is crucial to successful management of your organization. When uncertainty becomes resolved or known through the passage of time, actions, and events, decision makers can make the appropriate midcourse corrections by applying the knowledge gained and making decisions along flexible strategies. Integrated Risk Management (IRM) is a discipline that incorporates this learning model and permits the decision maker to take advantage of the full range of options, whereas traditional analyses that neglect this strategic flexibility will grossly undervalue certain capabilities, projects, and strategies. At the same time, advanced risk analytics, simulations, forecasting, and optimization techniques can be applied to obtain business intelligence for making better decisions.The IRM approach incorporates a learning model, such that management makes better and more informed strategic decisions when some levels of uncertainty are resolved or become known over time. The discounted cash flow analysis assumes a static investment decision, and assumes that strategic decisions are made initially with no recourse to choose other pathways or options in the future. To create a good analogy of IRM, visualize it as a strategic road map of long and winding roads with multiple perilous turns and branches along the way. Imagine the intrinsic and extrinsic value of having such a road map or global positioning system when navigating through unfamiliar territory, as well as having road signs at every turn to guide you in making the best and most informed driving decisions. This is the essence of IRM.

IRM is useful in valuing a decision through forecasting its strategic business options and risks, while mitigating any downsides and taking advantage of its upsides within the context of a portfolio of projects. For instance, should a firm invest millions in a new e-commerce initiative? How does a firm choose among several seemingly cashless, costly, and unprofitable information-technology infrastructure projects? Should a firm indulge its billions in a risky research and development initiative? The consequences of a wrong decision can be disastrous or even terminal for certain firms. In a traditional discounted cash flow model, these questions cannot be answered with any certainty. In fact, some of the answers generated through the use of the traditional discounted cash flow model are flawed because the model assumes a static, one-time decision making process while the real options approach takes into consideration the strategic managerial options certain projects create under uncertainty and management’s flexibility in exercising or abandoning these options at different points in time, when the level of uncertainty has decreased or has become known over time.

The answer to evaluating such projects lies in IRM, which can be used in a variety of settings, including pharmaceutical drug development, oil and gas exploration and production, manufacturing, e-business, startup valuation, venture capital investment, IT infrastructure, research and development, mergers and acquisitions, e-commerce and ebusiness, intellectual capital development, technology development,facility expansion, business project prioritization, enterprise-wide risk management, business unit capital budgeting, licenses, contracts, intangible asset valuation, and the like.

The IRM process is an 8-step quantitative software-based modeling approach for the objective quantification of risk (such as revenue projections, costs, investments, schedule uncertainty, market, development, technical, environmental, etc). The approach can be applied to: decision making, corporate investments, program management, resource portfolio allocation, portfolio project selection, return on investment, analysis of alternatives, strategic flexibility options, forecasting, prediction modeling, and general decision analytics. This methodology has been taught and applied by the author for the past 15 years at over 300 multinational corporations, and the author’s 12 books, software and methodology are used and taught at more than 300 universities globally.

The IRM Approach

The IRM approach is based on the 8-step process. Each step is modular and provides useful information for decision makers by itself and, when combined, provides a complete and comprehensive advanced decision-based risk analysis.

Step 1: Problem Definition and Risk Identification

Step 2: Prediction and Capability Analysis

Step 3: Return on Investment (ROI) Modeling

Step 4: Risk Simulation and Risk Quantification

Step 5: Framing of Strategic Alternative Flexibility Options

Step 6: Real Options Valuation

Step 7: Portfolio Optimization, Allocation, and Project Selection

Step 8: Iterative Program Management and Reallocation

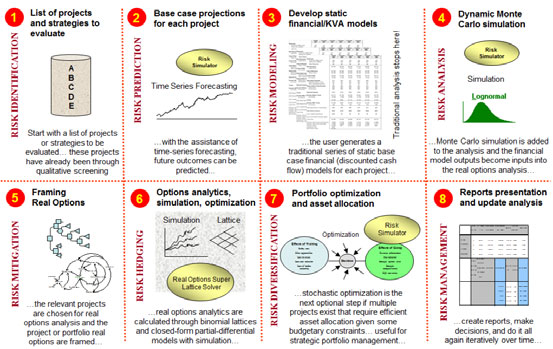

Figure 1 illustrates the eight-step process and where each step is modular and can be executed in isolation or in combination with any other step.

Figure 1: Integrated Risk Management Process

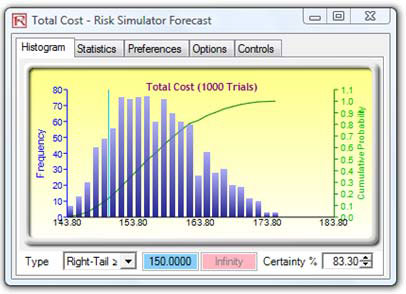

Figure 2 shows a sample risk simulation result, where revenue, cost, return on investment, schedule, technical, and other forms of risks can be simulated hundreds of thousands of times to understand the impact and characteristics of risks on a capability, project, and program. From this simulation, we can determine what the probability of success is or the probability that a certain variable like sales is obtained or chances of a schedule or budget overrun, and the results can be compared across multiple projects.

Figure 2: Quantitative Risk Analysis

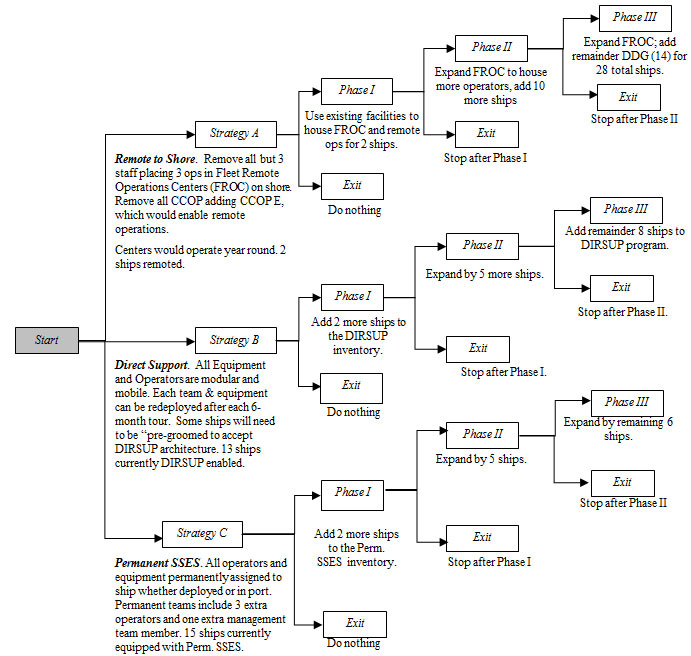

Figure 3 shows the analysis of alternatives analyzed through the framing of strategic flexibility and real options. Multiple pathways or alternatives are quantified––risk simulations of hundreds of thousands of alternatives are run, flexibility options are identified and valued.Each of the branches in the strategy tree is analyzed and valued, the net benefits are quantified, and the optimal decision pathway is then determined. Decision lattices are then built to find the optimal timing of execution and the value of flexibility options: options to wait and defer (value of information, proof of concept, right of first refusal), execute (build of buy), expand (platform technology, acquisitions, advanced concept technology demonstration, reusability, scalability), abandon (exit, salvage), contract (joint venture, partnerships), switch (modularity, redundancy, and sequential options (stage gate, milestones, planned product improvement, low rate initial production).

Figure 3: Strategic Analysis of Alternatives

Automobile and Manufacturing Industry

General Motors (GM) applies real options to create switching options in producing its new series of autos. This is essentially the option to use the cheaper resource over a given period of time. GM holds excess raw materials and has multiple global vendors for similar materials with excess contractual obligations above what it projects as necessary. The excess contractual cost is outweighed by the significant savings of switching vendors when a certain raw material becomes too expensive in a particular region of the world. By spending the additional money in contracting with vendors a meeting their minimum purchase requirements, GM has essentially paid the premium on purchasing a switching option. This is important especially when the price of raw materials fluctuate significantly in different regions around the world. Having an option here provides the holder a hedging vehicle against pricing risks.

Computer Industry

HP-Compaq used to forecast sales in foreign countries months in advance. It then configured, assembled, and shipped the highly specific configuration printers to these countries. However, given that demand changes rapidly and forecast figures are seldom correct, the preconfigured printers usually suffer the higher inventory holding cost or the cost of technological obsolescence. HP-Compaq can create an option to wait and defer making any decisions too early through building assembly plants in these foreign countries. Parts can then be shipped and assembled in specific configurations when demand is known, possibly weeks in advance rather than months in advance. These parts can be shipped anywhere in the world and assembled in any configuration necessary, while excess parts are interchangeable across different countries. The premium paid on this option is building the assembly plants, and the upside potential is the savings in making wrong demand forecasts.

Airline Industry

Airbus and Boeing spends billions of dollars and several years to decide if a certain aircraft model should even be built. Should the wrong model be tested in this elaborate strategy, Boeing’s competitors may gain a competitive advantage relatively quickly. Because there are so many technical, engineering, market, and financial uncertainties are involved in the decision making process, Boeing can conceivably create an option to choose through parallel development of multiple plane designs simultaneously, knowing very well the increasing development cost of developing multiple designs simultaneously with the sole purpose of eliminating all but one in the near future. The added cost is the premium paid on the option. However, Boeing will be able to decide which model to abandon or continue when these uncertainties and risks become known over time. Eventually, all the models will be eliminated save one. This way, the company can hedge itself against making the wrong initial decision, and benefit from the knowledge gained through parallel development initiatives.

Oil and Gas Industry

In the oil and gas industry, companies spend millions of dollars to refurbish their refineries and add new technology to create an option to switch their mix of outputs among heating oil, diesel, and other petrochemicals as a final product, using real options as a means of making capital and investment decisions. This option allows the refinery to switch its final output to one that is more profitable based on prevailing market prices, to capture the demand and price cyclicality in the market.

Telecommunications Industry

In the past, companies like Sprint and AT&T installed more fiber-optic cable and other telecommunications infrastructure than any other company in order to create a growth option in the future by providing a secure and extensive network, and to create a high barrier to entry, providing a first-tomarket advantage. Imagine having to justify to the Board of Directors the need to spend billions of dollars on infrastructure that will not be used for years to come. Without the use of real options, this would have been impossible to justify.

Utilities Industry

In the utilities industry, firms have created an option to execute and option to switch by installing cheap-to-build inefficient energy generator peaker plants only to be used when electricity prices are high and to shut down when prices are low. The price of electricity tends to remain constant until it hits a certain capacity utilization trigger level, when prices shoot up significantly. Although this occurs infrequently, the possibility still exists, and by having a cheap standby plant, the firm has created the option to turn on the switch whenever necessary, to capture upside price fluctuation.

Real Estate Industry

In the real estate arena, leaving land undeveloped creates an option to develop at a later date at a more lucrative profit level. However, what is the optimal wait time or the optimal trigger price to maximize returns? In theory, one can wait for an infinite amount of time, and real options provide the solution for the optimal timing and price trigger value. Pharmaceutical Research and Development Industry In pharmaceutical or research and development initiatives, IRM can be used to justify the large investments in what seems to be cashless and unprofitable under the discounted cash flow method but actually creates compound expansion options in the future. Under the myopic lenses of a traditional discounted cash flow analysis, the high initial investment of say a billion dollars in research and development may return a highly uncertain projected few million dollars over the next few years. Management will conclude under a net-present-value analysis that the project is not financially feasible. However, a cursory look at the industry indicates that research and development is performed everywhere. Hence, management must see an intrinsic strategic value in research and development. How is this intrinsic strategic value quantified? A real options approach would optimally time and spread the billion dollar initial investment into a multiple stage investment structure. At each stage, management has an option to wait and see what happens as well as the option to abandon or the option to expand into the subsequent stages. The ability to defer cost and proceed only if situations are permissible created value for the investment.

High-Tech and e-Business Industry

In e-business strategies, IRM can be used to prioritize different ecommerce initiatives and to justify those large initial investments that have an uncertain future. Real options can be used in e-commerce to create incremental investment stages compared to a large one-time investment (invest a little now, wait and see before investing more) and creates options to abandon and other future growth options. All these cases where the high cost of implementation with no apparent payback in the near future seems foolish and incomprehensible in the traditional discounted cash flow sense are fully justified in the real options sense when taking into account the strategic options the practice creates for the future, the uncertainty of the future operating environment, and management’s flexibility in making the right choices at the appropriate time.

Mergers and Acquisition

In valuing a firm for acquisition, you should not only consider the revenues and cash flows generated from the firm’s operations but also the strategic options that come with the firm. For instance, if the acquired firm does not operate up to expectations, an abandonment option can be executed where it can be sold for its intellectual property and other tangible assets. If the firm is highly successful, it can be spun off into other industries and verticals or new products and services can be eventually developed through the execution of an expansion option. In fact, in mergers and acquisition, several strategic options exist. For instance, a firm acquires other entities to enlarge its existing portfolio of products or geographic location or to obtain new technology (expansion option); or to divide the acquisition into many smaller pieces and sell them off as in the case of a corporate raider (abandonment option); or it merges to form a larger organization due to certain synergies and immediately lays off many of its employees (contraction option). If the seller does not value its real options, it may be leaving money on the negotiation table. If the buyer does not value these strategic options, it is undervaluing a potentially highly lucrative acquisition target.

Recent Comments